The Platform

Obsolete Appraisals of CRE Buildings: The Fifth Tsunami

06.17.2026

The next phase of the CRE crisis may stem from appraisals that ignore intelligent infrastructure.

When it comes to appraising commercial real estate (CRE) buildings, a fundamental question is increasingly difficult to ignore: how accurate are those valuations? How comprehensive are they? More importantly, do they account for the technologies and intelligent infrastructure that increasingly determine whether a building can attract tenants, generate revenue, and remain viable in a rapidly changing marketplace?

The answers to those questions are becoming more consequential by the day. What we are witnessing now may be the beginning of a Fifth Tsunami sweeping through commercial real estate markets, one that could have profound implications for property valuations, lending institutions, investors, and municipal economies.

Since 2020, commercial real estate across the United States has undergone a dramatic paradigm shift. The COVID-19 pandemic accelerated changes that many believed would take years to unfold. Instead, they arrived almost overnight. Remote work became a permanent reality for a significant portion of the workforce, creating a lasting bifurcation between employees who returned to offices and those who did not.

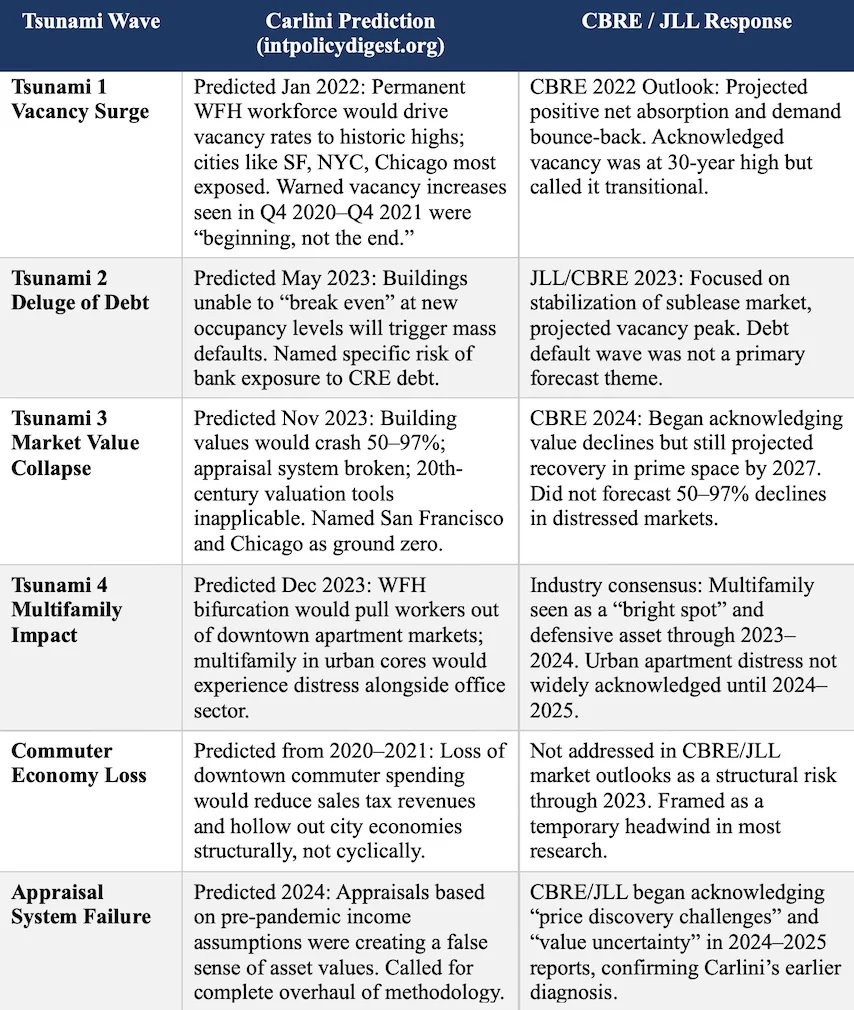

The impact was immediate and measurable. Most major cities experienced a 30 to 40 percent decline in daily commuter traffic. Office towers that once bustled with activity suddenly found themselves operating at a fraction of their former occupancy.

Yet many industry forecasts underestimated the permanence of the change. CBRE’s 2022 U.S. Real Estate Market Outlook acknowledged historically high vacancy rates but framed them as a transitional condition. JLL similarly projected stabilization and an eventual recovery in demand, anticipating positive net absorption as the year progressed.

That recovery never arrived.

What those forecasts failed to recognize was that only part of the workforce would return to office buildings. Millions of employees remained at home, not temporarily, but permanently. Rather than stabilizing, vacancy rates continued climbing through 2022 and 2023. By 2024, certain San Francisco submarkets were reporting vacancy rates exceeding 30 percent.

What those forecasts failed to recognize was that only part of the workforce would return to office buildings. Millions of employees remained at home, not temporarily, but permanently. Rather than stabilizing, vacancy rates continued climbing through 2022 and 2023. By 2024, certain San Francisco submarkets were reporting vacancy rates exceeding 30 percent.

The first four tsunamis that reshaped downtown districts and regional CRE markets since 2020 can be summarized as follows: The tsunami of surging vacancies; the tsunami of the deluge of debt; the tsunami of collapsing commercial property values; and the tsunami of declining multi-family property values.

These developments have been documented extensively in more than two dozen articles dating back to mid-2020, when corporations first began reassessing their space requirements. As work-from-home arrangements became entrenched, companies reduced their physical footprints dramatically. In many cases, firms cut leased office space by 50 to 80 percent compared to pre-pandemic levels.

The consequences are no longer confined to office properties.

Evidence is emerging nationwide that multi-family properties are facing similar pressures. According to a recent Nightingale Associates announcement, Scott Everett’s S2 Capital faces a $78 million foreclosure involving The Republic Apartments in Garland, Texas. Trinity Investors, which serves as the feeder fund for S2 Capital’s REIT, warned investors that they should expect a complete loss of capital.

Not long ago, REITs were widely regarded as relatively safe investments. Today, that assumption appears far less certain.

The value destruction occurring throughout commercial real estate is difficult to ignore. One recent example involved a 42,000-square-foot retail condominium at 99 Broadway in Manhattan’s SoHo district. Appraised at approximately $150 million in 2016, the property sold in 2026 with an appraised value of only $32 million, according to figures reported by FC Nightingale.

That represents nearly an 80 percent decline in value. For any portfolio owner holding such an asset, the loss is staggering.

Another example comes from Austin, Texas. The Line Austin, a luxury hotel overlooking Lady Bird Lake near South Congress Avenue, has reportedly been flagged for a foreclosure auction following a default on a $172 million loan issued by JPMorgan in 2023. The future valuation of the property remains uncertain, but it illustrates the mounting pressures confronting even high-profile assets.

As noted in earlier analyses, leasing office space increasingly resembles a reverse game of musical chairs. The number of available seats continues to rise while the number of players continues to shrink.

This imbalance has concentrated remaining demand within Class A properties while many Class B buildings struggle to achieve occupancy levels necessary for profitability. Some analysts continue to argue that demand will eventually migrate back into older properties. That expectation may prove misplaced.

Demand today is increasingly driven by operational requirements rather than location alone. Organizations seeking space often require facilities capable of supporting mission-critical applications, advanced communications systems, and uninterrupted operations.

Many existing buildings simply cannot provide those capabilities.

A technologically obsolete building often lacks redundant electrical systems, resilient broadband connectivity, advanced monitoring capabilities, and the digital infrastructure necessary for modern enterprises. Without substantial investment, such properties become increasingly difficult to lease regardless of location.

There is an important distinction between renting space and renting intelligent space.

Traditional office space has become a commodity. In commodity markets, landlords compete primarily on price, frequently undercutting one another to secure tenants. Intelligent space operates differently. Buildings equipped with resilient infrastructure, advanced connectivity, smart building systems, and enhanced operational capabilities offer unique value that cannot easily be replicated.

As a result, owners of such properties are not necessarily forced into a race to the bottom on rental rates.

This raises uncomfortable questions for lenders and portfolio managers.

Many financial institutions appear reluctant to fully confront the implications of changing property values. The reason is understandable. If a portfolio is believed to be worth $5 billion, few stakeholders welcome a reassessment that might reveal its actual value to be a fraction of that amount.

Yet the market eventually forces reality into the conversation.

The true appraisal of a commercial building should include the value of the intelligent infrastructure it provides. If those technological capabilities are excluded, the resulting valuation may be incomplete and potentially misleading.

A building that cannot support modern business requirements may possess little value beyond the land on which it sits. In such cases, the structure itself becomes obsolete, regardless of how impressive it may appear from the street.

Many portfolio managers understandably do not want to hear that conclusion. Some are quietly attempting to dispose of underperforming assets before further declines occur. Others may still be carrying what could be described as “ghost equity”—paper valuations that no longer reflect market realities.

New questions therefore need to be addressed by property owners, investors, lenders, and management firms.

Can technology investments increase a building’s appraised value? If they can, why are they not receiving greater attention during underwriting and valuation processes?

One recent example demonstrated how reducing a building’s water expenses by approximately $30,000 annually resulted in an estimated $4 million increase in appraised value. If a relatively straightforward efficiency improvement can generate such a result, what other technology investments might materially enhance property values?

“There are eight cranes on my one-square-mile island, North Bay Village,” notes Darrin Mylet, CEO of Telosa Networks in Miami. Development activity there remains robust.

As Mylet puts it, “Capital follows common sense.”

In his view, investors gravitate toward markets that balance reasonable government oversight with predictable regulations rather than excessive bureaucracy, restrictions, and costly red tape.

The contrast with many traditional urban centers is striking. In some high-growth regions, cranes dominate the skyline. In others, development activity has slowed considerably. Downtown Chicago, for example, continues to face significant challenges absorbing existing office inventory. New construction is difficult to justify when large quantities of vacant space remain available.

Technologically obsolete buildings are not attracting new tenants. As corporate leasing footprints continue to shrink, vacant space often remains vacant because it lacks the intelligent amenities and infrastructure modern organizations require.

Developers and investors are also increasingly attentive to governance, regulatory stability, and infrastructure resilience when evaluating potential projects. Capital tends to avoid markets characterized by dysfunction, uncertainty, or ineffective leadership.

Successful commercial real estate projects require more than attractive architecture and favorable demographics. They depend upon reliable power, resilient broadband connectivity, and the intelligent infrastructure necessary to support modern business operations.

Until developers, local governments, lenders, and property management firms collectively recognize the realities of a permanently divided workforce, market volatility is likely to persist. The commercial real estate industry is operating within a fundamentally different environment than the one that existed before 2020.

That reality demands a new framework for assessing value.

Technology is no longer a peripheral feature of commercial buildings. It has become one of the essential building blocks upon which future property performance depends.

Given what intelligent infrastructure provides—redundant power systems, resilient connectivity, operational sensors, and enhanced building management capabilities—it should occupy a central role in both building assessments and appraisal methodologies.

Ignoring those factors risks producing valuations that belong to the past rather than the market that exists today.

James Carlini is a strategist for mission critical networks, technology, and intelligent infrastructure. Since 1986, he has been president of Carlini and Associates. Besides being an author, keynote speaker, and strategic consultant on large mission critical networks including the planning and design for the Chicago 911 center, the Chicago Mercantile Exchange trading floor networks, and the international network for GLOBEX, he has served as an adjunct faculty member at Northwestern University.